Enhance the personal banking experience through system thinking

A digital payment solution designed for a regional bank to modernize personal banking experiences. The product supports both mobile and non-mobile users by enabling secure, cardless ATM transactions and alternative digital payment methods. Built with accessibility, security, and user inclusivity at its core, the solution streamlines payment workflows for customers and support agents while ensuring compliance with industry standards.

The bank's existing cash withdrawal system relies heavily on physical cards and in-person interactions, limiting accessibility for users with mobile devices who expect faster, more secure digital options. This dependency creates friction in everyday banking, particularly at ATMs, where mobile-first customers lack alternative ways to access their funds. Additionally, internal support teams face growing inefficiencies due to redundant workflows and fragmented systems.

This solution brought together a complex network: mobile and non-mobile users, ATMs, the bank’s app and web platform, support agents, developers, and compliance teams. Each had a unique role, from enabling cardless withdrawals to ensuring security and seamless support. Our goal was to align this system behind one unified, intuitive user experience.

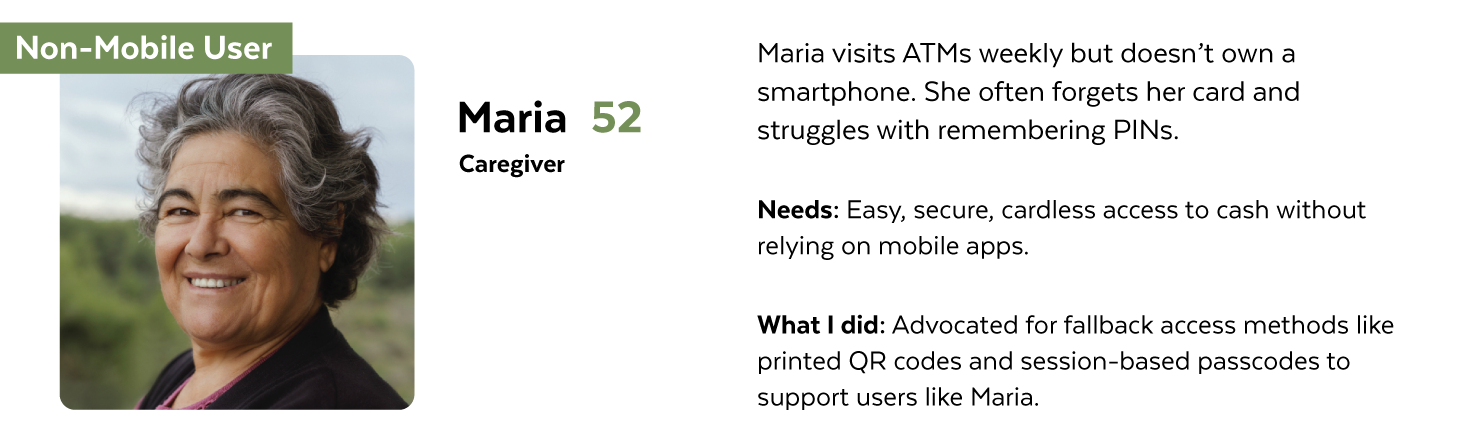

To guide our decisions, I created composite personas based on user research, usability findings, and internal team insights. One key persona emerged:

When I joined the project, I reviewed past decisions and conducted interviews with mobile and non-mobile users. I observed ATM uses data and spoke with support agents to uncover hidden pain points. This research revealed key themes that shaped our personas and guided the design toward accessibility, clarity, and trust.

Mobile-first users were frustrated by the continued need for physical cards.

Non-mobile users felt excluded from new digital workflows and overwhelmed by ATM complexity.

No support for cardless ATM withdrawals

Despite relying on their phone, users still needed a physical card to withdraw cash.

Inconsistent app-to-ATM experience

The mobile app didn’t integrate smoothly with ATM workflows, causing friction.

Security concerns around mobile transactions

Users worried about exposing sensitive info if the mobile flow wasn’t airtight.

Dependency on physical cards

If users forgets or loses their card, they have no alternative way to access funds.

Confusing ATM workflows

Cluttered screens and unclear steps make ATM use stressful, especially without digital assistance.

Lack of secure fallback options

One-size-fits-all security methods don’t work well for users without mobile devices.

Guided by user research and real-world pain points, I focused on designing solutions that balanced accessibility, security, and ease of use. Each solution targeted a specific user need that ensuring both mobile-first and non-mobile users could access their funds confidently and intuitively.

To address problems such as card dependency, inconsistent ATM flows, and security concerns, I created a smooth cardless experience for mobile users. In just a few simple steps, users select their account, tap to authenticate, choose withdrawal or deposit options, confirm amounts, verify with biometrics, and complete the transaction quickly, securely, and easily.

To make deposits easier and smoother, I created a cardless process that helps mobile users move from the app to the ATM clearly. Users choose their account in the app, tap to verify at the ATM, insert cash or cheques, and confirm the amount, all without a physical card. This process is secure, simple, and reduces steps while maintaining accuracy and control.

To make sure users without smartphones can access services, I created a secure, cardless experience using an NFC-enabled access card. This physical card lets users tap at the ATM to log in without a mobile app. The process includes essential actions like withdrawing, depositing, and paying, with extra safeguards such as PIN verification for large transactions and session timeouts to prevent misuse. This solution provided non-mobile users equal access to modern banking without sacrificing security or ease of use.

With research insights in hand, I led collaborative sessions to explore solutions from both technical and user perspectives. The goal was to generate ideas that balanced real-world constraints with user needs which focusing on accessibility, cardless access, and security.

I started with quick, low-fidelity sketches to explore different directions for cardless ATM access and simplified workflows. These rough ideas helped me validate core concepts early, prioritize key interactions, and get fast feedback from the team before moving into wireframes.

Building on the lo-fi sketches, I created mid-fidelity wireframes to map out the full experience. This included mobile authentication, ATM interaction, and fallback options for non-mobile users. The wireframes helped align layout, content hierarchy, and user flow across different scenarios.

After validating the wireframes, I created detailed user flows to ensure clarity across all key actions, including withdrawing, depositing, and paying. These flows showed how users would move through each step, starting a transaction on the app and completing it at the ATM. For non-mobile users, the flows illustrated how they could access services using an NFC-enabled access card. This process also helped identify edge cases, security checkpoints, and backend dependencies early on.

With the user flows defined, I translated them into high-fidelity designs to bring the experience to life. I focused on creating a clean, accessible interface that reflected the bank’s brand while ensuring clarity across mobile and ATM screens. For mobile users, I designed a secure and intuitive cardless flow. For non-mobile users, I integrated clear prompts for using the physical card tag. Each screen was refined through internal reviews and prepared for usability testing.

After creating the detailed designs, I focused on improving the visual style and interaction flow of the mobile app. This involved using consistent spacing, typography, icons, and motion to make things clear and help users complete tasks such as withdrawing, depositing, and paying. I also made sure the design followed accessibility guidelines, ensuring the experience was inclusive and easy to navigate for both mobile and non-mobile users.

The redesigned experience improved user engagement and operational efficiency. After the launch:

Cardless transactions increased by 40% in the first 3 months, showing strong adoption from mobile users.

Support requests related to ATM access dropped by 25% due to simpler flows and clearer user guidance.

Transaction completion time decreased by an average of 30 seconds, making high-frequency actions like withdrawals and deposits faster.

Non-mobile user access grew with the introduction of NFC-enabled cards, allowing more people to participate without needing smartphones.

These results helped the bank progress towards its digital transformation goals while reducing friction, improving security, and addressing a wider range of user needs.

This project deepened my understanding of designing for inclusivity for both mobile and non-mobile users. I learned how to turn complex banking tasks into simple, secure flows by working closely with developers and compliance teams.

If I were to do it again, I’d push for earlier usability testing, especially at the mid-fidelity stage. This would help validate assumptions faster and improve interactions with more user feedback. Overall, it was a valuable reminder that great design solves real problems when based on research, accessibility, and trust.